In the U.S., we have decided, through the laws created by our elected officials, that individual taxable income should be taxed at progressive rates. In other words, the more taxable income you have, the bigger percentage of that income you have to pay in taxes.

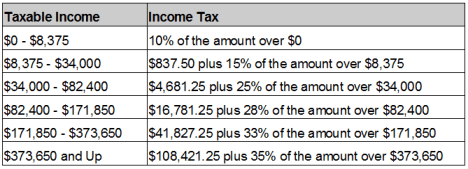

To attempt to simplify the application of this approach, the lawmakers created income ranges that are taxed at different rates, creating tax brackets. Based on current laws, taxable income (i.e. amount reported on line 43 of Form 1040) ranging from $0 to $8,375 by a single tax filer is taxed at a rate of 10%. The income reported from $8,375 to $34,000 by this same single filer is taxed at a higer rate of 15%. Here are the 2010 tax brackets for single filers:

2010 Federal Income Tax Brackets for Single Filers

Brief History of U.S. Tax Brackets

Since 1913, when the federal income tax was made permanent, we have had tax brackets. Our first set of brackets was fairly simple, with rates ranging from 1% to 7%. This initial set of brackets applied to all tax filers. In the 40s and 50s, different tax brackets were created for Single, Married Filing Jointly, Married Filing Separately, and Head of Household.

The highest federal tax rate ever levied in the U.S. was a whopping 94% for income over $200,000 back in 1944 and 1945. Tax rates and income brackets can change each year, based on new law and inflation adjustments.

“What Tax Bracket Am I In?”

One of the most common questions tax filers have is, “what tax bracket am I in?” We already know, based on the brackets above, that every filer is effectively in every tax bracket, up to their highest. So we can assume that the question really is, “what is my highest tax bracket?” The rate associated with your highest bracket is actually called your marginal tax rate. For instance, if you make $90,000 in 2010, you will have a 28% marginal tax rate.

Does this mean that you will pay 28% of $90,000 in taxes for the year? No. It just means that the highest margin of income you report will be taxed at 28%. This is useful because generally every dollar you add to your current income will be taxed at that highest rate. Likewise, every reduction you make (i.e. tax deductible expense) will generally save you that percentage in tax dollars.

What you might be more interested in knowing though is your effective tax rate. This is the percentage of your taxable income that was actually paid in taxes. To determine your effective tax rate from last year, find your tax return and divide your total tax by your taxable income. Think of this as your average rate across all brackets.