One of the most challenging periods in life can be the loss of a spouse. During such an emotionally difficult time, tax and financial implications are likely the last things on your mind (and understandably so).

That said, it’s also important to make sure you remain financially secure. Understanding the qualifying surviving spouse filing status can help ease your tax burden after the loss of a spouse.

In an effort to reduce the complications caused by the need to deal with federal and state tax issues following a loved one’s passing, TurboTax has compiled a list of tax items to keep in mind when you file as a surviving spouse.

Table of Contents

What does the qualifying surviving spouse filing status mean?Who qualifies as a qualifying surviving spouse?Tax advantages of the qualifying surviving spouse filing statusShould you file as single or qualifying surviving spouse?What does the qualifying surviving spouse filing status mean?

Qualifying surviving spouse, once termed qualifying widow(er), is a tax-filing status that allows a surviving spouse to benefit from the same tax rates as married couples filing jointly, for up to two years after the year of their spouse’s death.

To put it simply, if your spouse passed away, you may still be eligible to continue filing your taxes in a similar manner as prior to the loss for up to three years, including the year of death.

The qualifying surviving spouse filing status helps ease the financial burden by providing a lower tax rate compared to filing as a single taxpayer.

Why filing status matters

To maximize tax benefits and minimize your liability, it’s important to choose the best filing status available to you. Your filing status determines your filing requirements, tax rate, and your standard deduction.

As long as you do not get remarried the same year, you are allowed to file a joint tax return with your spouse in the year of their death. Typically, the married filing jointly status will give you the largest tax benefit.

Who qualifies as a qualifying surviving spouse?

The qualifying surviving spouse filing status is a tax status allowing you, as the surviving spouse, to file taxes with the same tax breaks as if you’re still married. Through this filing status, you benefit from joint return rates up to two years after the year of your spouse’s death.

Here’s how to qualify:

Joint return eligibility

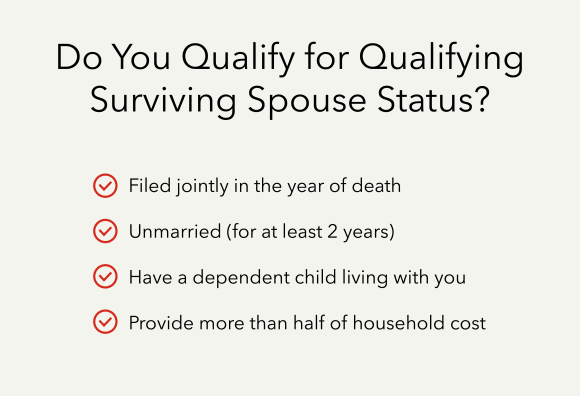

To qualify for this tax status, you must be eligible to file a joint return with your spouse in the year of their death.

Remarriage

One of the requirements to be eligible to use the surviving spouse filing status is that you remain unmarried. If you remarry before the two-year period after the year of your spouse’s death, you lose eligibility for the qualifying surviving spouse filing status.

Dependents

Another stipulation for qualifying for this tax filing status is that you must have a dependent child who lives with you for more than half of the year. The child must also be under the age of 19 or a full-time student under the age of 24. Dependents can be your:

- Biological child

- Stepchild

- Legally adopted child

Residence and home costs

Finally, you need to have provided more than half of the costs of maintaining your household. Residence and home costs include:

- Rent

- Mortgage

- Utilities

- Groceries

- Other necessary living costs

In addition, your home must be the primary residence of the dependent child (excluding temporary absences).

Tax documents

To claim this filing status, you’ll need to provide a few tax documents. These could include:

- Your deceased spouse’s final tax return

- Proof that you are the custodial parent of your dependent child

- Evidence of the home and living expenses

Proper documentation is essential in order to prove that you meet all qualifications. Having this information accessible also makes filing your taxes easier.

Tax advantages of the qualifying surviving spouse filing status

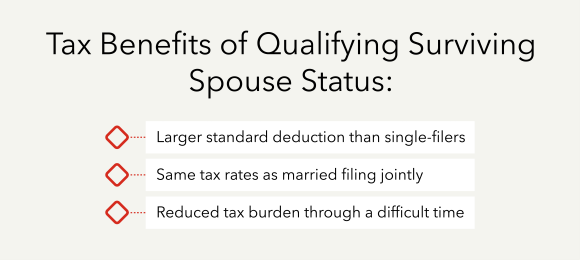

Filing under the qualifying surviving spouse filing status provides several tax advantages, including access to beneficial rates and deductions typically reserved for married couples filing jointly. Therefore, this tax filing status can help reduce the tax burden during a difficult time.

Standard deduction

One of the most beneficial advantages of the qualifying surviving spouse filing status is that you get the same standard tax deduction as married filing jointly status.

This is the largest standard deduction and was set at $29,200 for married couples filing jointly in 2024. In 2025, the standard deduction for married couples filing jointly will increase to $30,000.

In contrast, the standard deduction in 2024 for single filers was $14,600 and is set at $15,000 for 2025. Taxpayers that file as qualifying surviving spouse benefit from a significantly larger standard deduction.

Property and assets

If your spouse owned property that you inherit, the inherited portion of that property receives a “stepped-up basis.” In community property states, the entire asset is stepped-up. This means that when you sell that property, instead of using the original cost as the cost basis, you can use the fair market value at the date of death.

This usually lowers the capital gain you may need to claim in the year of the sale of the property due to post-death appreciation of the property.

If you and your spouse owned the property as community property, then both halves of the property get the stepped-up basis (not just the half that they owned). This concept also applies to any other assets owned, such as real estate, stock, and/or mutual funds.

There are special rules that govern if you and your spouse owned rental property. Since it qualifies for a step-up in tax basis to its value at the date of their death, you can use that increased tax basis for depreciation purposes as well.

This will reduce your taxable income because you will get to take more of a depreciation expense until the rental property is fully depreciated or you sell it.

Social Security

Another area that’s impacted is Social Security retirement benefits. As a widow/widower, you’re now eligible to collect full benefits based on your deceased spouse’s earnings record if those benefits are greater than the benefits you were collecting as your own.

You can collect reduced widow benefits as early as age 60, or wait and collect full benefits at full retirement age. Whichever age you choose to start collecting, don’t forget that Social Security may not deposit the full amount of those benefits into your bank account since monthly benefits are often reduced by the cost of Medicare premiums.

Should you file as single or qualifying surviving spouse?

When it comes to filing your taxes, how do you decide between single and qualifying surviving spouse status? Well, it’s important to consider the tax benefits and how each status impacts your tax bracket and overall financial situation.

Filing as a qualifying surviving spouse allows you to take advantage of a larger standard deduction and more favorable tax rates, similar to married filing jointly. Filing as single results in a smaller standard deduction and higher tax rates.

If you meet the criteria, such as having a dependent child and not remarrying, it’s typically a more advantageous choice to file as a qualifying surviving spouse when you plan for taxes.