While not everyone needs to go to college to have a successful career, many people want to pursue higher education. If you’re a parent or guardian caring for children, you may want to think about starting a college fund for your kids.

The earlier you start saving, the more time your money has to grow through compound interest. Even small, regular contributions can add up over time. Having a dedicated college fund for your kids can give you peace of mind, knowing that you are preparing for their future.

While the idea of financial planning for college might make you anxious, there are plenty of small but significant steps that you can take to begin the process and ease the burden in the future.

With a bit of planning, you can turn small contributions into big financial and educational gains. Every little bit counts, and starting now can make a big difference down the road.

Let’s explore your savings options so you can get a better understanding of the benefits of each and make informed decisions that best suit your family’s needs.

What are your options for building a college fund for your kids?

If you’re ready to save for your child’s educational future, you’ll want to consider all the different avenues of college funds to find the right one for you. The most popular and tax-advantaged option is often the 529 savings plan, but you’ll find that there are other savings accounts worth exploring as well.

Let’s break down some of the most popular savings options.

529 savings account

529 accounts are state-sponsored investment accounts designed specifically for college savings for students. Today, most states offer at least one type of 529 plan. Most states don’t require you to be a resident to open a 529 account there, so you can compare different plans and make a decision accordingly.

Some of the key features of 529 accounts include:

- Tax-free growth: Money in 529 plans grows tax-free while it remains in the account.

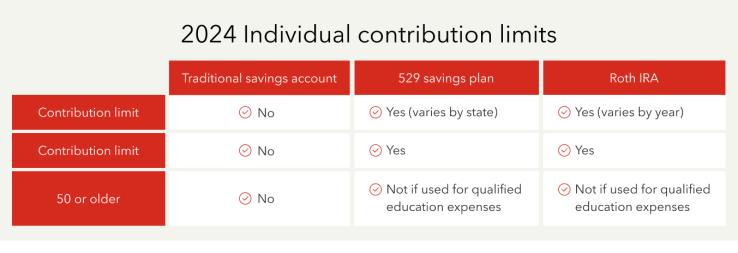

- High contribution limits: Contribution limits for 529 plans vary by state. For example, in California, the contribution limit is currently $529,00, while it’s $475,000 in Alabama and $235,000 in Mississippi.

- State tax benefits: Many states offer state income tax deductions or credits for 529 plan contributions.

- Flexible use: Use 529 funds for any qualified education expense. Verify if an expense qualifies to avoid income tax and a 10% penalty on withdrawals.

- No withdrawal limit for college expenses: There’s no limit on withdrawals for qualified college expenses.

Many plans also accept third-party contributions, allowing anyone to contribute to your kid’s college fund. When determining financial aid eligibility, qualified withdrawals from 529 accounts do not count as income. However, the FAFSA application includes funds in 529 plans as part of their calculation of parental assets.

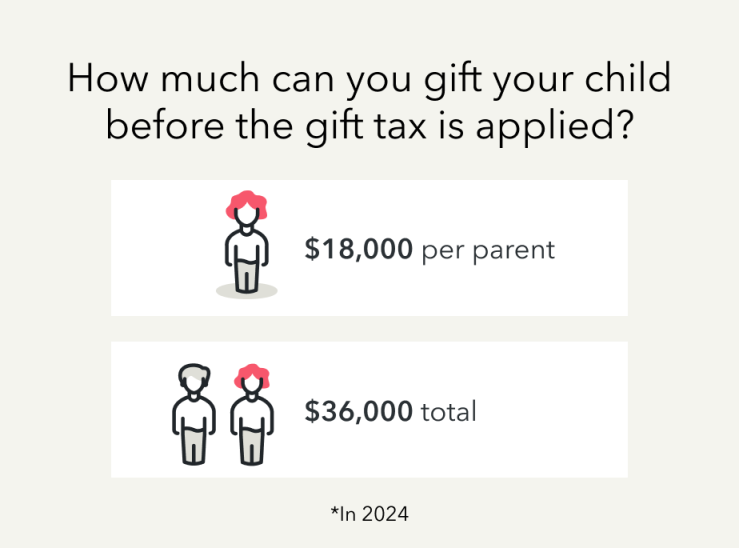

When considering whether a 529 plan is right for you, it’s important to note that it might qualify for the gift tax. For 2024, you can contribute up to $18,000 (or $36,000 if married) to one 529 account per year and remain under the reporting requirement.

Roth IRA

IRAs are individual retirement accounts, and Roth IRAs are a popular type of IRA because of their tax-free growth. They can also be used to pay for college expenses. If you already have a Roth IRA that you’ve been contributing to over the years, you may find it easier to continue using that account as a college fund for your kids rather than opening new accounts.

You can withdraw Roth IRA contributions anytime to use for qualified education expenses tax-free and without paying a penalty. You can also use Roth IRA earnings for educational expenses tax-free and without penalty, but if you do so before 59 ½ years of age, that amount will be subject to income tax.

Annual contribution limits for Roth IRAs are much lower than 529 plans, with a limit of $7,000 or $8,000 for those 50 or older, but if you’re going to be saving for many years, this may not be an issue for you.

Savings account

Don’t forget about traditional savings accounts! While they typically provide a lower return on your investment compared to 529s and IRAs, they may still be a good option, depending on your situation.

Traditional savings accounts are easy to set up and manage, and you can withdraw funds at any time for any purpose without incurring penalties. There are usually no contribution limits, and your money is typically FDIC-insured, providing higher security. Additionally, the money in a traditional savings account isn’t subject to market fluctuation, so you don’t have to worry about losses during economic downturns.

The main drawback? Low interest rates mean your money won’t grow as significantly over time, and any interest you earn is subject to state and federal income tax.

When should you start a college fund for your kids?

When it comes to savings, the sooner, the better. Starting a college fund for your child when they are born allows more time for the savings to compound interest. However, any savings are better than none, so go ahead and start that college fund if you still have time.

You can even open a college fund account before your child is born. If you want to open a 529 account for your future child, you can name yourself as the beneficiary and transfer it to your child when they arrive.

How much should you invest in a college fund for your kids?

Let’s first look at tuition prices. For the 2023-2024 school year, average tuition in the US was:

- $42,162 for private universities

- $23,630 for out-of-state students at public universities

- $10,662 for in-state students at public universities

Multiply these numbers by four or five years, depending on the program, and you’re looking at a substantial amount. Don’t forget to calculate estimates for room and board, books, and other living costs for a student budget.

When choosing specifically how much to invest, you’ll want to factor in the following:

- Future cost of tuition: University tuition has historically gone up about 8% annually, so you’ll want to estimate the cost based on the year your child will likely go to college.

- Number of children: The more kids you have, the more money you’ll likely need to save.

- Time until college: The older your child is, the more aggressive your savings strategy needs to be. For example, if your child is 13, you’ll want to invest more in a shorter period of time compared to starting a fund for an infant.

- State schools vs private universities: If you anticipate your child attending a private university, you’ll want to save more than for an in-state public university based on the differences in expected costs.

A common savings goal is to cover a third of the total projected cost with the expectation that future income, scholarships, and financial aid can help cover the rest. That said, you can reduce the risk of struggling to afford your child’s education if you save more.

How do you withdraw the money from your kid’s college fund when the time comes?

For 529 accounts:

- Time your withdrawal accordingly

- Request to withdraw your designated amount

- Have it sent directly to the university, the beneficiary, or your personal account

- Keep your receipts to prove that the money was used for qualified educational expenses

Remember, qualified expenses include tuition, fees, books, supplies, and equipment required for enrollment. Room and board also qualify if the student is enrolled at least half-time. Computer equipment and internet access used primarily for education can also be covered.

It’s important to plan your withdrawals strategically. For 529 plans, consider using them for larger expenses like tuition while using other funds for smaller costs. This helps you maximize the tax benefits of your plan.

For Roth IRAs and traditional savings accounts, you’ll just withdraw the necessary funds when the time is right. Just remember to keep receipts for purchases made with Roth IRA contribution withdrawals so you can prove to the IRS that the funds were used for qualified educational expenses. Otherwise, it will be subject to income tax and a 10% penalty. Remember, any purchases made with Roth IRA earnings will still be subject to income taxes if they are made before you reach 59 ½ years old.

6 Tips for building a college fund for your kids

Need some help when it comes to maximizing your child’s higher education fund? These tips can help you maximize their college fund:

1. Start early

At the risk of overstating it, the sooner you start saving, the more time your money has to grow.

2. Automate it

Set up automatic monthly contributions to your kid’s college fund so you won’t have to think twice about it.

3. Hire your kids:

If you are self-employed or own a business, you may want to consider employing your children and putting a portion of the earnings into their college funds. You can also deduct their wages as a business expense, but keep accurate records and make sure they do real work.

4. Educate your child about college costs

Help them understand the expenses early on. They may consider in-state schools or help save if they want the more expensive option. You can also teach them about the various tax savings for students.

5. Get family and friends involved:

You can encourage family members or friends to donate to your kid’s college fund as part of their gifts for occasions such as birthdays, graduations, and more.

6. Get professional advice:

If you find yourself confused or overwhelmed by setting up a college fund for kids, you may want to consult a financial advisor. They can help you choose the best-suited accounts and strategies for your situation.

No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.