You may be wondering if it’s too early to start preparing for tax season. The answer is no. You should be preparing for tax filing throughout the year.

The thought of filing can feel overwhelming for many business owners, but with a little preparation, you can put your mind at ease. From important documents and forms to deadlines, we’ve created a comprehensive business tax checklist to simplify the process.

Whether you’re a seasoned entrepreneur or a first-time filer, this business tax checklist will empower you with the knowledge and tools needed to succeed.

Say goodbye to chaotic crunch time before filing, and hello to a more organized, streamlined filing experience. Let’s dive into this small business tax prep checklist.

Table of Contents

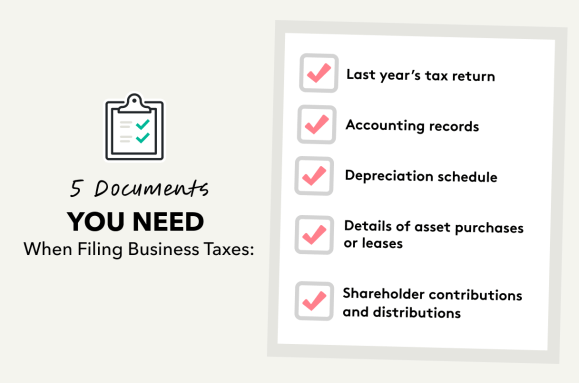

5 Types of documentation you should have on hand to file Details of asset purchases or leasesWhen should business owners start tax planning?More Tips for Preparing for Tax SeasonWhen are business taxes due?5 Types of documentation you should have on hand to file

Make filing a breeze this year by gathering the right documentation ahead of time. For new businesses and established enterprises alike, it’s vital to keep clean books and prepare ahead of time.

An overview of documentation should be at the top of your small business tax checklist. Here are five essentials you should have on hand to make filing more efficient:

Last year’s tax return

This form is essential for referencing as it provides a foundation for your current filing. Last year’s tax return can help you quickly identify any changes in income or deductions.

It will also help you easily track any carryover items from previous years, such as net operating losses, capital losses, or unused tax credits that may still apply. By comparing last year’s return to your current filing status, you can ensure accuracy and spot potential tax-saving opportunities.

Accounting records

Your accounting records are critical to your business’s financial health. This includes profit and loss statements showing your income and expenses, balance sheets reflecting your overall financial position, and cash flow statements highlighting the movement of cash in and out of your business.

Accounting records give you a comprehensive view of your financial activities, allowing you to accurately report income and expenses while identifying potential deductions and write-offs. Organized accounting documents also help you avoid errors in tax reporting and support any claims in the event of an audit.

Depreciation schedule

Your depreciation schedule outlines the value of your business assets over time, detailing how much you can deduct from your taxable income based on wear and tear. This is particularly important for long-term investments like equipment, vehicles, and buildings that can’t be deducted in a single year.

This schedule shows exactly how much you’ve already deducted and how much remains for future tax years. Have your depreciation schedule ready for filing season to ensure you’re not leaving money on the table.

Details of asset purchases or leases

When filing taxes, it’s important to have records of any asset purchases or leases. When you start a business, make sure to keep invoices, contracts, and payment records so you can accurately report these transactions. Proper documentation is key for tax filing to ensure you have a paper trail for anything you’re trying to claim.

Filing your taxes often depends on providing proof of your expenditures. Some assets may qualify for Section 179 deductions, allowing you to deduct the full purchase price upfront. Others may need to be depreciated over time, as detailed above.

By keeping detailed records, you’ll be prepared for potential audits and equipped to take advantage of any potential opportunities.

Shareholder contributions and distributions

If your business is structured as a corporation or partnership, keeping detailed records of shareholder contributions and distributions is crucial. Contributions refer to any investment capital from shareholders. Distributions represent earnings or profits paid out of contributions.

By clarifying ownership stakes, you can avoid potential disputes or misreporting and ensure accurate reporting and compliance.

When should business owners start tax planning?

Don’t put off your tax planning until crunch time. The best time to start tax planning is to do it continuously throughout the year. By proactively managing your tax strategy throughout the year, you can better position your business for financial success.

Planning for tax filing involves more than just crunching numbers in the final weeks before the deadline. It requires you to consider how your tax obligations will influence your business decisions. For example, the type of entity you choose can significantly impact your liability when it comes to taxes.

Throughout the year, tax planning can help you identify opportunities to optimize your financial position. A holistic approach to your financial operations ensures that you make informed decisions leading you to sustainable growth and profitability.

More Tips for Preparing for Tax Season

By adopting proactive strategies, you can prepare your business to tackle tax season with ease. From getting your tax forms in order to keeping detailed records, here are some valuable tips to help you optimize your tax situation:

Create a plan for filing taxes

Make tax season easier than ever by establishing a clear timeline. Set deadlines for yourself for gathering documents, completing forms, and submitting your return. Reduce stress by setting goals so you can file small business taxes with plenty of time to spare.

Choose the best business entity for your organization

Different types of business entities affect your taxes in different ways. This can range from sole proprietorship to partnership, LLC, or corporation. Each entity type has its own tax structure, benefits, and drawbacks. That’s why it’s important to weigh the pros and cons of each type for your situation.

Keep detailed records

The best thing you can do for your business is to maintain accurate and organized records of all your financial transactions. From income to expenses, invoices, receipts, and bank statements, detailed records simplify the tax preparation process.

Plan to maximize deductions and credits

There are various deductions and tax credits designed to help your business. Do your research to see which ones your business qualifies for, such as the home office deduction, and develop a strategy to maximize these deductions.

Keep business and personal expenses separate

This may go without saying, but be sure to keep your business and personal expenses separate. Use dedicated bank accounts and credit cards to track business expenses so it’s clear which deductions you can make for your business.

Contribute to a retirement plan

Making contributions to retirement plans like a 401(k), SEP IRA, or SIMPLE IRA, can reduce your taxable income. By setting aside pre-tax income into a retirement plan for yourself and your employees, you reduce the amount of tax you owe for the year.

It can also provide valuable savings for the future, making it an effective tax planning strategy to consider. Employers can typically deduct contributions made on behalf of their employees, reducing their business’s overall tax bill.

Work with a tax professional to prepare and file

Still, a bit intimidated by the tax filing process? The good news is you don’t have to face filing taxes alone. While preparing and filing taxes on your own is doable, working with a tax professional can lighten the load. A tax expert can help you navigate complex tax laws and ensure that you maximize deductions.

Tax professionals can also provide tailored advice based on your business’s unique needs and situation. If you’re looking for a blend of convenience and expert assistance, TurboTax Live Business offers the best of both worlds.

With TurboTax Live, you can connect with tax experts for personalized advice and even have them review or file your return or do everything on your behalf.

When are business taxes due?

Key dates and timelines are an integral part of your small business tax prep checklist. The deadlines for filing taxes vary depending on your business type. Make sure to note these deadlines for tax returns and payments to avoid penalties and interest.

- Individuals: Income tax returns, including those reporting 1099 Form income, are typically due on April 15 of each year. If the 15th falls on a weekend or holiday, the deadline will be adjusted. For those who need more time, an extension can be filed by your tax deadline to give you until October 15.

- Sole proprietorships and single-member LLCs : These entities file taxes along with the personal income tax deadline of April 15.

- S-Corps: These corporations must file their returns using Form 1120-S by March 17.

- C-Corps: These entities typically have to file by April 15 for those on a calendar-year basis. However, if your C-Corp follows a different fiscal year, your return is due on the 15th day of the fourth month following the end of your fiscal year.

Don’t forget that your business may also need to make estimated tax payments throughout the year to avoid being fined. Estimated quarterly payments are generally* due on the following days:

- April 15

- June 15 (June 16, 2025)

- September 15

- January 15

*If the due date falls on a weekend or holiday, payment is due on the following non-holiday business day.

By making quarterly payments, you’ll stay current with your tax obligations and avoid penalties for underpayment.

Mark these deadlines on your calendar to ensure timely filing and payment. This will make your filing process easier and keep your business in good standing with the IRS. By following this small business tax checklist, you’ll stay ahead of the game and tackle your taxes with confidence.