Selling your home comes with a pretty long to-do list, including familiarizing yourself with tax requirements.

Whether you’re a first-time seller or a seasoned homeowner, navigating the complexities of taxes and selling your home is essential to maximizing your profits and reducing the risk that you’ll owe unexpected taxes.

From capital gains tax exemptions to deductions for home improvements, being informed can make a significant difference in your bottom line.

Let’s explore eight essential tips to help you navigate the tax landscape when selling your house, ensuring you make the most of your investment while staying compliant with tax regulations.

Table of Contents

Key takeaways Find out if you?re eligible for the primary residence exclusion.Don?t forget to account for home improvements. Realtor and lender fees can reduce your bottom line and taxes. Reporting might not be necessary.Research state-specific tax considerations.Understand how much of the property taxes you?re liable for.Learn how to calculate capital gains taxes for selling your home.Plan ahead for tax season.Key takeaways

- You might be able to avoid capital gains tax on a home sale if you qualify for a home sale tax exclusion or primary residence exclusion.

- Taxpayers in all 50 States have to pay property tax, but rates may vary.

- Property tax divides the tax responsibilities proportionally based on the time each party owns the property during the tax year.

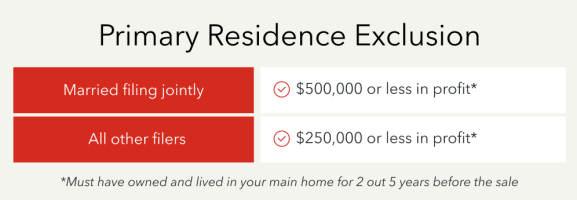

Find out if you’re eligible for the primary residence exclusion.

When selling your principal residence, one thing to keep in mind is all the money you earn from the sale may be tax-free. If you owned and lived in it as your main home for two out of five years before the sale, you can make up to $250,000 profit on your home sale, and you may not have to claim it on your taxes.

If you’re married, your exclusion gets more of a boost. As a married couple filing a joint tax return, you may be able to exclude up to $500,000 profit from the sale.

Don’t forget to account for home improvements.

If you enhanced your home with improvements like a new roof, a remodeled kitchen, or a full-on backyard remodel with a pool, don’t forget to add what you paid for your home improvements to your home’s cost basis (what you paid for it) to get the adjusted basis.

Increasing your cost basis by what you paid for your home improvements to arrive at your adjusted basis will lower your taxable gain.

For instance, if you sold your house for $500,000 and paid $200,000 for it, you may think your gain is $300,000, but by making sure you add your $100,000 in home improvements, you will reduce your profit below the taxable level to $200,000.

Realtor and lender fees can reduce your bottom line and taxes.

Realtor sales commissions and points you pay on behalf of the seller can really add up, but you can lower your profit by making sure you decrease the proceeds from the sale by any sales commissions paid or points paid on behalf of the seller.

Reporting might not be necessary.

If you’re lucky enough to sell your home and make a profit, you may find, like the majority of taxpayers, that you don’t need to report your home sale when it’s time to file your taxes thanks to the gain exclusion rules in place unless you receive Form 1099-S, Proceeds from Real Estate Transactions.

You can avoid getting this form if you certify (usually at closing) that you meet the ownership, use, and timing tests.

Ownership

Five years prior to the date of the sale, you must have owned the home for at least two years. That said, those two years don’t have to be continuous or immediately preceding the sale of your home.

Use

The home you’re selling must have been used as your primary residence for at least two of the five years prior to the date of the sale.

Timing

You haven’t claimed the exclusion on a sale of another home within the last two years prior to this sale.

Research state-specific tax considerations.

When it comes to real estate transactions, taxpayers in all 50 States and Washington, D.C., have to pay property tax.

Property tax is a tax on real property (land and buildings, both residential and commercial). This tax is primarily imposed by local governments such, as cities, countries, and school districts, rather than state governments. That said, states may have overarching laws that dictate how taxes apply to personal property.

Real estate transfer taxes, also known as recordation tax, conveyance tax, or deed stamp tax, are taxes imposed on the transfer of real property from one individual or entity to another.

These local transfer taxes generally are in addition to any applicable state-level transfer taxes, and a majority of states provide for this tax.

For example, in Washington, D.C., the state transfer tax is 1.1% of the fair market value of the property if it’s less than $400,000, and 1.45% if it’s greater than $400,000. Meanwhile, California has $1.1 per $1,000 of value, or 0.11% of the selling price for a state transfer tax.

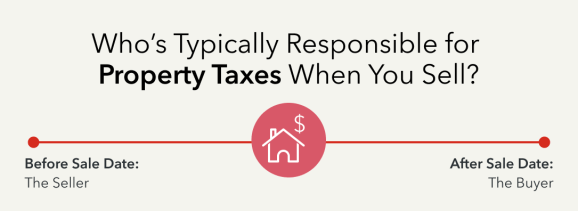

Understand how much of the property taxes you’re liable for.

Property tax is assessed based on your primary residence, second home, rental property, and other real estate you own.

It plays a pivotal role when it comes to taxes for selling your home, by serving as a fair method to allocate property tax responsibilities between the buyer and the seller (you).

Property taxes are paid annually, but when a property changes hands, it wouldn’t be equitable for only one party to shoulder the entire tax burden for the year.

So, for property taxes, the tax obligation is divided proportionally based on the time each party owns the property during the tax year.

This means that real estate sellers (you) are responsible for taxes up to the sale date, and the buyers are responsible for taxes from the sale date moving forward.

Learn how to calculate capital gains taxes for selling your home.

Capital gains tax on the sale of a house depends on the amount of profit you make from the sale and is defined by the difference between how much you paid for the house and how much you sold it for.

Luckily, like the majority of taxpayers, you may qualify for the primary residence exclusion, which means you won’t need to report your home sale when it’s time to file your taxes.

Feel confident about your tax responsibility when you sell your home with our free capital gains tax calculator.

Plan ahead for tax season.

Plan ahead for taxes and selling your house, and get the most out of your tax deductions by keeping detailed records of eligible expenses and home improvements.

If you sell your house this year, there’s no need to worry about knowing these rules. TurboTax will ask you simple questions and give you the tax deductions you are eligible for based on your answers.