Planning for retirement is a great way to stay ahead of the game, but what do you do when you find a new job and start investing in a separate retirement plan?

401(k) rollovers allow you to transfer the funds from your old 401(k) to a new retirement plan or account. If you’re changing jobs or switching from a 401(k) to an IRA, a rollover can be a smart choice.

If you’re making changes in your life and considering rolling over a 401(k), we’re here to help. Keep reading to learn how to rollover a 401(k), what your options are, and whether a 401(k) rollover is right for you.

Table of Contents

What does it mean to roll over a 401(k)?Options for your 401(k) rolloverCan you keep your 401(k) with your old employer?How long do you have to roll over your 401(k)?What are the pros and cons of a 401(k) rollover?What are the pros and cons of cashing out a 401(k)?What does it mean to roll over a 401(k)?

When you get hired, your employer might ask if you want to start a 401(k). These tax-advantaged accounts can help you save for retirement, so they’re a common benefit offered by companies.

If you get a new job, your new employer may also offer a 401(k). In this scenario, many people would choose to rollover their current 401(k) from their old employer to their new employer. Rolling over your 401(k) means moving the funds from that old account into the new one, and then closing the previous 401(k).

Alternatively, you can also roll your 401(k) over into a traditional or Roth IRA so you have more investment choices.

With a rollover, the idea is that you keep all your money in one place, which is often easier to manage for most people. In some cases, rollovers may be optional, but in others, it’s required.

Options for your 401(k) rollover

Let’s take a look at some of the things you can do with your 401(k) savings.

Roll your 401(k) over to your new employer

When you’re hired by a new employer, you can keep your 401(k) with your old employer or roll it over to your retirement plan or account with your new employer.

Before you decide to roll your 401(k) over to your new employer, check the costs, features, and rules of your new plan. If you don’t like the investment choices your new plan offers, you might want to stick with your old 401(k).

Your new 401(k) may also have different withdrawal rules, which can affect when you’re able to withdraw your money and whether withdrawals are penalized.

If you’re not sure how to roll over your 401(k) to a new employer, you can usually contact your plan provider for guidance.

Roll your 401(k) over to an IRA

If you want more control when saving for retirement, you can roll your 401(k) over to an individual retirement account (IRA).

When you decide to roll your 401(k) over to an IRA, you can choose between a traditional IRA and a Roth IRA. Roth IRA withdrawals are typically tax- and interest-free after age 59½, while traditional IRA withdrawals are taxed as current income.

Because you’re paying taxes on Roth IRA contributions right now, your contributions are taxed at your current tax rate. Traditional IRA withdrawals are taxed as income, so your tax liability may increase if you’re in a higher tax bracket when you make withdrawals.

Since Roth IRA contributions are made with after-tax dollars, you can’t deduct your contributions on your taxes. If you opt for a traditional IRA, you may be able to deduct your contributions at the end of the year.

Rolling your 401(k) over to an IRA can give you more control and investment choices, but you’re responsible for deciding how to invest. You can also work with a financial advisor to make sure you’re making smart investments.

While 401(k) vs. IRA tax benefits are similar, there are several key differences. Before you roll your 401(k) over to a Roth or traditional IRA, make sure it’s the right option based on your circumstances.

Can you keep your 401(k) with your old employer?

When you start a job with a new employer, you don’t necessarily have to roll your 401(k) over to your new employer. You can choose to roll your 401(k) over to a Roth or traditional IRA — or you may be able to keep your 401(k) with your old employer.

Check with your employer to see if you’re allowed to leave your money in your 401(k) after changing jobs. Some 401(k) accounts have a force-out provision where you have to withdraw or rollover your money unless you meet a certain balance threshold.

If you decide to keep your money in your old 401(k), you can’t keep contributing to that plan. Your plan provider can also increase the cost of your plan since you’re not an employee anymore.

Managing multiple tax-deferred accounts can be a challenge if you keep your 401(k) with your old employer. You have to take required minimum distributions (RMDs) starting at age 73, and you may face penalties if you don’t take your RMD on time.

The good news is that you maintain the freedom to withdraw from your old 401(k) or roll the funds over at any point in time. If you decide you want to roll your 401(k) over to an IRA or employer-sponsored plan, you can.

If you’re not sure whether to keep your 401(k) with your old employer, ask your financial advisor how to roll over a 401(k) to a new employer and whether that’s the right solution for you.

How long do you have to roll over your 401(k)?

The process of rolling over your 401(k) varies based on the type of rollover you choose — a direct rollover, a trustee-to-trustee transfer, or a 60-day rollover.

With a direct rollover, your plan administrator can distribute your money in the form of a check made out to your new account. The IRS won’t withhold any taxes from your direct rollover.

A trustee-to-trustee allows the financial institution managing your retirement plan to make a direct payment to another retirement plan. This is a simple way to roll over to a new account, and no taxes will be withheld.

If you’re not keeping your 401(k) with your old employer and opting for a 60-day rollover, you’ll receive a distribution from your old account. Once you receive this distribution, you have 60 days to roll those funds over to another 401(k) or IRA.

In some cases, the IRS may waive the 60-day rollover requirement.

60-day rollovers are also subject to tax withholding, which means you’ll have to use additional funds to roll over the complete amount.

The IRS also has a one-per-year rule, which means you can’t make more than one rollover from the same retirement account in a 1-year period.

What are the pros and cons of a 401(k) rollover?

Whether you have a 401(k) for self-employed people or a plan through your employer, rolling over your 401(k) is a big decision. Weighing the pros and cons can help you make the right choice for you.

Rolling over your 401(k) to your new employer can make it easier to manage and monitor your funds since they’re all in one place. If you continue to work for that employer, RMDs can even be delayed beyond age 73 and can be delayed until you retire.

You can also choose to roll your 401(k) over to a traditional or Roth IRA, giving you more investment choices. Rolling your 401(k) over to a Roth IRA can also offer tax benefits when you decide to retire.

The downside of a 401(k) rollover is that your new employer’s plan may be worse. Potential downsides may include less favorable investment choices, higher plan costs, and stricter withdrawal rules.

If you roll your 401(k) over to an IRA, those funds may no longer be eligible to roll over into a 401(k). You’ll either need to hire a financial advisor or make your own investment choices.

Rolling your 401(k) over can also affect self-employed taxes.

What are the pros and cons of cashing out a 401(k)?

You may be considering cashing out your 401(k) for various reasons. You can cash out a 401(k) instead of rolling it over, but it’s important to understand the effects of cashing out.

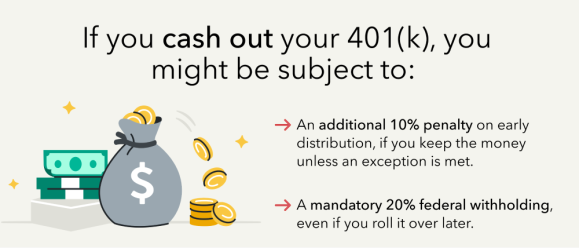

The biggest benefit of cashing out your 401(k) is liquidity. Cashing out your 401(k) gives you access to cash, and you can withdraw without early withdrawal penalties if you leave your job during or after the year you turn 55.

If you cash out and don’t move your money into a qualified retirement plan, the funds are taxed as income, and you may face an additional 10% penalty. All 401(k) withdrawals are subject to mandatory 20% federal withholding.

If you are under 55 ½ years old, you may be able to qualify for an exception to the 10% additional tax on early distribution if you meet any of these exceptions.

No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.