Debt can have a significant impact on your emotional and financial health, so it’s only natural that you’d want to get out of debt by any means necessary.

If you’re having a difficult time getting out from under that pile of bills, you may be considering using a 401(k) to pay off debt. While strategies like this can be effective, it’s also important to understand the potential risks.

Learn more about paying off debt with your 401(k). We’ve put together a few money management tips to help you make an informed decision.

Table of Contents

Key takeawaysCan I use my 401(k) to pay off debt?What are the potential benefits of cashing out your 401(k) to pay off debt?What is the penalty for withdrawing your 401(k) early?What are the other disadvantages of withdrawing from your 401(k) early?What is the difference between a 401(k) withdrawal and a 401(k) loan?Alternative methods to consider for paying off debtsKey takeaways

- You can make an early withdrawal from your 401(k) to pay off debt.

- Using early withdrawals to pay off debt may make sense in some scenarios.

- Early 401(k) withdrawals face a 10% penalty and additional income taxes on the amount distributed.

- You can make penalty-free early withdrawals if you qualify for an exception.

Can I use my 401(k) to pay off debt?

Technically speaking, cashing out a 401(k) to pay off debt is an option. You can withdraw money from your 401(k) at any point in time, but that doesn’t mean it’s necessarily the best decision based on your financial situation.

If you’re new to having a 401(k), you may want to consult a financial advisor before you make any major decisions. Your advisor can give you personalized advice based on your financial situation.

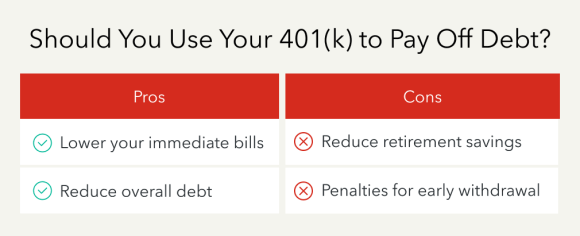

What are the potential benefits of cashing out your 401(k) to pay off debt?

While it’s not necessarily a good idea for everybody to cash out a 401(k) to pay off debt, there are times when it makes sense. It’s important to consider the value of your retirement account, your income, and the amount of debt you have.

If you have a massive amount of debt with high interest, making a 401(k) withdrawal to pay off debt could make sense.

While there is a penalty for making an early withdrawal from your 401(k), that penalty might be lower than the interest you’d incur over the course of several months or years.

Understandably, paying off debt as soon as possible is usually preferable, but you don’t want to sacrifice your greater financial stability or future to pay off debt.

What is the penalty for withdrawing your 401(k) early?

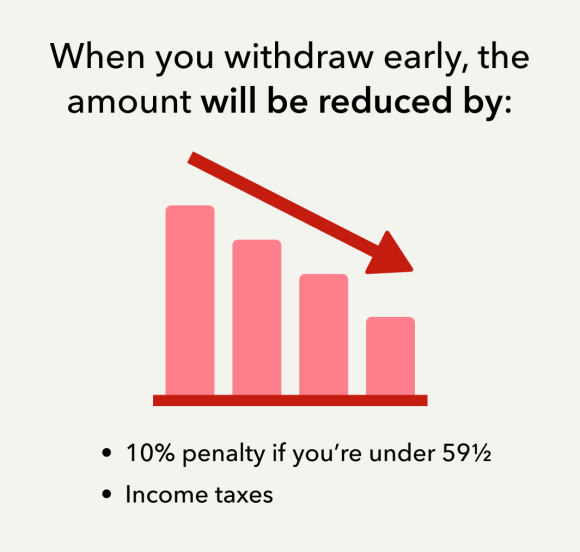

When you have any type of retirement plan, it’s important to understand the rules. Retirement accounts incentivize planning for the future, so withdrawing money before you retire typically comes with a penalty.

If you withdraw from your 401(k) before you turn 59½ years old, you’ll typically face a penalty equal to 10% of the amount of the withdrawal. You’ll also have to pay your current income tax on any money you withdraw from your 401(k).

When you wait until 59½ to withdraw from a 401(k), you typically have less taxable income. This results in lower income tax rates, which means you can save on income taxes and avoid penalties when you wait until you’re eligible to withdraw.

It’s also important to note that there are exceptions to the 59½ rule for 401(k) withdrawals. Some exceptions include:

- Unreimbursed medical expenses (over 7.5% of AGI)

- Health insurance premiums while unemployed

- First time homebuyers (withdrawal up to $10,000)

- Withdrawing after leaving your job at age 55 or older (50 or older for certain public safety employees)

- Substantially equal periodic payments (SEPP)

- Terminal illness

- Total and permanent disability

If you choose to leave your job at age 55, you can only make penalty-free withdrawals from the 401(k) you set up through that job. If you have any other 401(k) plans, you have to wait until you’re 59½ or qualify for an exception to make a withdrawal.

The “rule of 55” also doesn’t apply if you have a 401(k) and are self-employed. If you’re no longer working and contributing to a solo 401(k), the plan will end.

What qualifies as a “hardship withdrawal”?

While the IRS typically discourages people from making early withdrawals from 401(k) accounts, participants may be allowed to take a hardship withdrawal.

If you’re using the money to cover certain expenses that are considered an “immediate and heavy financial need” and your distribution is limited to the amount necessary to satisfy such financial need, you can usually take a hardship withdrawal from your 401(k).

Hardship distributions are typically allowed for you, your spouse, your dependents or your primary beneficiaries to cover items such as:

- Medical expenses

- Funeral expenses

- Tuition and other education expenses

- Purchase of a principal residence

- Payments necessary to prevent eviction or foreclosure

- Costs to repair damage to your principal residence

Using hardship distributions to cover emergency expenses can help when you really need it, but there are some things to consider:

- Your hardship distribution reduces the total amount in your retirement account, which affects your retirement savings.

- Any untaxed money you receive as a hardship distribution will be taxed at your regular income tax rate.

- Unless you’re 59½ or qualify for an exception, you may still face a 10% penalty.

Like any financial decision, it’s important to weigh your options before deciding to receive hardship distributions.

You may also want to consult a professional who can help you choose the best course of action based on your finances and provide practical retirement tips.

What are the other disadvantages of withdrawing from your 401(k) early?

The biggest and most immediate disadvantage of withdrawing from your 401(k) is the cost. Not only do you have to pay a 10% penalty, but early withdrawals are also taxed at your current income tax rate — which is higher than it will be when you retire.

Let’s say you withdraw $10,000 from your 401(k). You’ll face a 10% penalty of $1,000, plus you’ll be taxed at your current income tax rate. That additional $10,000 is added to your taxable income, which means you could also land in a higher tax bracket.

Another huge disadvantage of using a 401(k) withdrawal to pay off debt is that it negatively impacts your retirement savings. Each early withdrawal reduces your total savings, so you’ll have less when you retire.

Unless a financial expert recommends using your 401(k) to pay off debt or cover emergency expenses, you’re better off maximizing your retirement savings and planning for the future.

What is the difference between a 401(k) withdrawal and a 401(k) loan?

Depending on the type of employer-sponsored plan you contribute to, you may be allowed to take out a 401(k) loan instead of making a withdrawal from your 401(k).

Loans are an option if you don’t want to pay penalties and additional taxes on early withdrawals.

Not all employer-sponsored plans offer 401(k) loans, and maximum loan amounts vary. Per the IRS, you can borrow the lesser of:

- $10,000 or 50% of your vested account balance or

- $50,000

Generally speaking, you have up to five years to pay back your 401(k) loan with interest. Each time you make a payment, that money goes back into your retirement account — so you’re not reducing your total savings by taking out a loan.

One key thing to remember is that 401(k) loans are attached to your employer. If you leave or lose your job before paying off your loan, you may have a shorter period to repay your loan.

If you can’t repay it, there are consequences. The portion of your loan you’re unable to pay will be considered a distribution from your 401(k), which means the early withdrawal penalties and additional taxes will apply.

Alternative methods to consider for paying off debts

Whether you have credit card debt, student loan debt, or medical debt, there are strategies you can use to start paying off those debts and eventually become debt-free.

Before you make an early withdrawal from your 401(k), explore some of these strategies.

Debt consolidation is one way to start managing your debt. Many people have various types of debt, which means they have to make several monthly payments to make sure they do not default on any loans.

Instead, you can consolidate all your debt into a single loan and a single monthly payment. This makes it easier to pay down your debt each month, and you may be able to negotiate better loan terms with a debt consolidation lender.

Budgeting is another way to start lowering your debt. Create a budget with your monthly income and expenses, then find areas where you can cut back. You can use the money you save by cutting back to pay your debts off faster.

You can also negotiate interest rates depending on your situation. If you can’t seem to get out ahead of loan or credit card interest, try negotiating a lower rate with your lender.